Investing in AXIS Capital Holdings Limited: A Discounted Stock with Strong Growth Potential and Attractive Dividend Yield

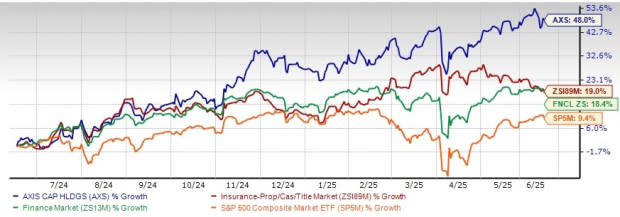

AXIS Capital Holdings Limited (AXS) has been a standout performer in the past year, gaining 48% compared to the 19% growth of its industry, the 18.4% growth of the Finance sector, and the 9.4% growth of the Zacks S&P 500 composite. The insurer has a market capitalization of $8.13 billion and an average volume of shares traded in the last three months of 0.7 million.

AXS has a solid track record of beating earnings estimates in each of the last four quarters, with an average of 13.89%. The company's shares are trading at a discount compared to the industry, with a forward price-to-book value of 1.51X, lower than the industry average of 1.56X and the Zacks S&P 500 Composite's 8.04X. AXS also has a Value Score of A and is cheaper compared to The Travelers Companies, Inc. (TRV), Arch Capital Group Ltd. (ACGL), and American Financial Group, Inc. (AFG).

The stock is trading above both its 50-day and 200-day simple moving averages, indicating solid upward momentum. The Zacks Consensus Estimate for AXS's 2025 earnings per share indicates a year-over-year increase of 3.4%, with a consensus estimate for revenues of $6.58 billion, implying a year-over-year improvement of 7.8%. The consensus estimate for 2026 earnings per share and revenues indicates an increase of 8% and 7.8%, respectively, from the corresponding 2025 estimates.

Each of the four analysts covering AXS has raised estimates for 2025, and one analyst has raised the same for 2026 over the past 60 days. The Zacks Consensus Estimate for 2025 and 2026 earnings has moved up 2.4% and 0.5%, respectively, in the past 60 days. Based on short-term price targets offered by eight analysts, the Zacks average price target is $112.38 per share, suggesting a potential 9.1% upside from the last closing price.

AXIS Capital's return on equity in the trailing 12 months was 19%, better than the industry average of 7.8%. The company aims to be a leading specialty underwriter and focuses on growth areas such as wholesale insurance and lower middle markets. Its strategic initiatives have been driving improvement in its operating earnings over the past few years, and it stays focused on expanding digital capabilities to create new business growth in desirable smaller accounts.

Axis Capital's dividend track record is impressive, with a dividend hike for 18 straight years and currently yielding 1.7%, way above the industry average of 0.2%. The insurer boasts one of the highest dividend yields among its peers.

In conclusion, AXIS Capital Holdings Limited is poised for growth with its focus on prudently deploying resources while enhancing efficiencies, improving its portfolio mix and underwriting profitability. The company has a VGM Score of A, indicating a potential upside and instilling confidence in investors. Higher return on capital, favorable growth estimates, and attractive valuations should continue to benefit Axis Capital over the long term. The stock currently carries a Zacks Rank #3 (Hold).