OppFi’s OPFI customer-centric approach serves as its paramount differentiator within the alternative lending platform market. While most players vie for market share, OppFi’s priority toward customer experience, trust and financial inclusion sets it apart.

OPFI’s bank-partner model is a key enabler of this customer-centric approach. This model targets the population that falls in the Fair Issac Corporation score range below the 650 mark, wherein traditional lending options get blurry. Hence, this practice allows the company to broaden its reach across the United States, ensuring a significant number of underserved consumers can access credit.

OppFi’s ability to serve customers is greatly improved by its advanced AI and machine learning models. In the first quarter of 2025, OPFI saw its auto-approval rate rise to 79% from 73% in the same quarter last year. This demonstrates an efficient application process, reducing friction and allowing qualified borrowers to access funds quickly. Besides effective cost management, the increasing auto-approval rate indicates faster decisions and a smoother experience for customers.

The tangible results from the customer-first strategy are evident in OPFI’s astounding customer satisfaction ratings. As of the first quarter of 2025, OPFI’s OppLoans had a 4.7/5.0-star rating on Trustpilot from more than 4,900 reviews, making the company one of the top consumer-related financial platforms online. Per Better Business Bureau, the company is rated A+, bolstering OppFi’s credibility and commitment to resolving customer issues.

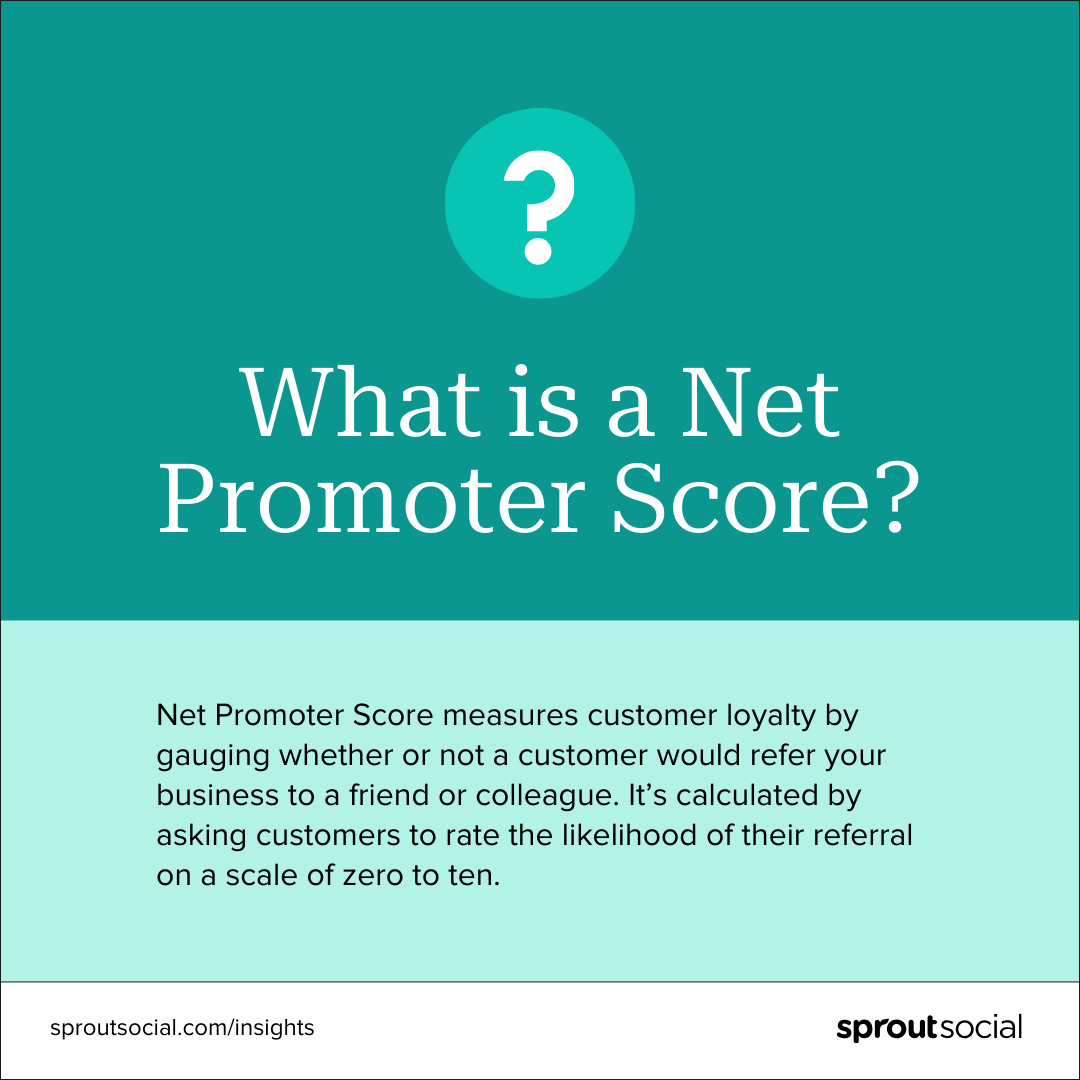

OppFi’s Net Promoter Score (NPS) is 78, signifying a highly loyal consumer base willing to advocate for its brand. These numbers collectively demonstrate OPFI’s commitment to transparency, simplified installment loans and features including same-day funding. It translates directly into customer loyalty and reputation, which serves the company well in distinguishing itself within the underserved population.

With the U.S. alternative lending platform market anticipated to grow, seeing a CAGR of 25.4% from 2025 to 2030, OPFI has positioned itself on the back of its elite customer-centric approach to enjoy a headstart in the race to capture a greater market share.

OPFI’s Price Performance, Valuation & Estimates

The stock has skyrocketed 297.4% in the past year, significantly outperforming its competitors, PayPal Holdings PYPL and Paysafe Limited PSFE, and the industry as a whole. The industry has rallied 28.1%. PayPal Holdings has gained 28.6%, while Paysafe Limited has declined 26.8% in the same period.

繼續閱讀

Zacks Investment Research

Zacks Investment Research Image Source: Zacks Investment Research

From a valuation standpoint, OPFI trades at a forward price-to-earnings ratio of 10.62, lower than the industry’s 22.84. PayPal and Paysafe trade at 13.86 and 4.95, respectively.

P/E - F12M

Zacks Investment Research Image Source: Zacks Investment Research

OPFI and Paysafe have a Value Score of A, whereas PayPal has a Value Score of B.

The Zacks Consensus Estimate for OppFi’s earnings for 2025 is pegged at $2.38 per share, suggesting 11.2% year-over-year growth.

Zacks Investment Research Image Source: Zacks Investment Research

OPFI currently flaunts a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

PayPal Holdings, Inc. (PYPL) : Free Stock Analysis Report

Paysafe Limited (PSFE) : Free Stock Analysis Report

OppFi Inc. (OPFI) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks Investment Research

![Executing a successful demand generation strategy [with examples]](https://www.antiochtenn.com/zb_users/upload/2025/07/20250703050158175149011834765.jpg)