Pinterests Expansion Plans and Margin Challenges: Can It Buck the Trend?

Pinterest, Inc. (PINS) is a leading player in the digital advertising industry, generating significant revenues through its website and mobile applications. The company is well-positioned to help advertisers reach the millennial and Gen Z audience, who are more active on immersive mobile platforms. However, despite healthy demand trends, net sales are often affected by seasonality, and the recovery of the digital ads market remains uneven. Additionally, Pinterest's global presence exposes it to foreign exchange fluctuations.

The company expects operating expenses to increase substantially in the near term as it expands operations both domestically and internationally, enhances its product offerings, broadens its user and advertiser base, expands marketing channels, hires additional staff, and develops new technology. Increased infrastructure spending related to user and engagement growth is likely to result in higher costs of revenue. In the first quarter of 2025, total costs and expenses increased 12.1% year over year, owing to higher research and development expenses. Our estimate for total costs and expenses for the June quarter is pegged at $937.7 million, implying year-over-year growth of 7.1%.

Investing in User Engagement and Monetization

Pinterest is prioritizing investments to augment user engagement and monetization, such as improving visual search capabilities and enhancing the technology that underpins ad-serving efficiency. The company has also begun testing productivity tools to automate repetitive tasks and standardize content for the sales force, allowing sellers to spend more time with clients. Although these initiatives are likely to affect near-term profitability, they are expected to help reach long-term margin goals.

Comparison with Other Tech Firms

In contrast, Snap Inc. (SNAP) is affected by lackluster user growth as it primarily focuses on the younger demographic and fails to attract the older generation (above 35-year-olds). Moreover, lack of revenue diversification is a major concern for Snap, as advertising is its only source of revenues, which is suffering from a continuous decline in price per ad impression. Similarly, Meta Platforms, Inc.'s (META) focus on Reels, which generates lower revenues than Stories and News Feed, has affected profitability to some extent. As the company continues to ramp up investments in products such as Video, AR/VR, and AI, costs are on the rise, hurting margins.

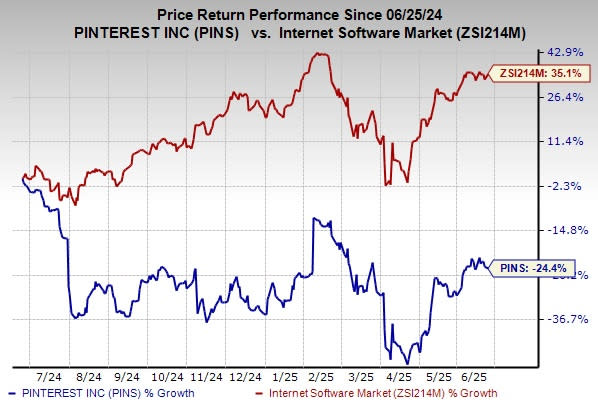

Valuation and Estimates

Pinterest has declined 24.4% over the past year against the industry's growth of 35.1%. From a valuation standpoint, Pinterest trades at a forward price-to-sales ratio of 5.2, below the industry average. The Zacks Consensus Estimate for Pinterest's earnings for 2025 has increased over the past 60 days. Pinterest currently carries a Zacks Rank #3 (Hold).

In conclusion, Pinterest is a strong player in the digital advertising space with significant growth potential. However, investors should be aware of the increased costs and potential near-term profitability challenges associated with its expansion plans and investments in user engagement and monetization. Despite these challenges, Pinterest remains well-positioned to capitalize on the growing demand for immersive mobile platforms among millennials and Gen Z users.