Realty Income Stock: Is It Still a Good Investment in 2025? A Look at Performance, Headwinds, and Valuation

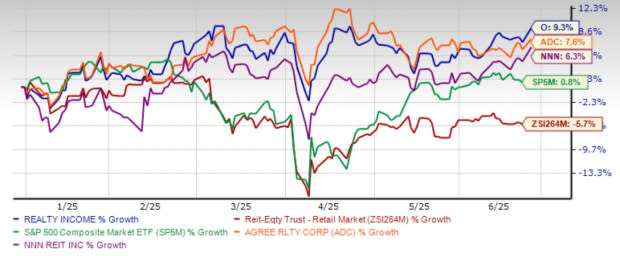

Realty Income Corporation (O) has delivered a solid 9.3% year-to-date (YTD) return, outpacing its peers and the broader market. The company's strategic investments in the United States and Europe, combined with its disciplined acquisition strategy and focus on quality assets, have contributed to its strong performance. However, investors are now questioning whether the stock remains attractively valued or if a better entry opportunity lies ahead. Realty Income stands out as a resilient and dependable REIT, offering stability and consistent income for fixed-income investors. Its evolution from a traditional net lease operator to a diversified, multi-sector global player has enhanced its long-term appeal. With 15,627 income-producing properties across the United States and Europe, the company focuses on non-discretionary retail and service-based tenants, which typically perform well through economic cycles and resist e-commerce pressures. The company's disciplined acquisition strategy and focus on quality assets have helped it consistently achieve high occupancy rates, with a historical median of 98.2%, surpassing the industry norm. As of March 31, 2025, occupancy remained robust at 98.5%, and management projects a continued rate above 98% for the year. Realty Income's strategic expansion, particularly in Europe and into growth sectors like gaming and data centers, signals a forward-looking growth trajectory. In the first quarter of 2025, it invested $1.37 billion at a 7.5% yield and targets $4 billion for the year. With an estimated $14 trillion global net lease market and a projected $4 billion in 2025 investments, Realty Income is positioning itself for long-term growth. Supported by strong financials, investment-grade credit ratings, a 5.63% dividend yield, and a history of consistent payouts, Realty Income remains a dependable option for income investors. Known as "The Monthly Dividend Company," this member of the S&P 500 Dividend Aristocrats has made 111 straight quarterly increases. Its latest and 131st dividend hike since its 1994 NYSE debut is payable on July 15 to shareholders of record as of July 1. However, while Realty Income has many strengths, it also faces meaningful headwinds. Macroeconomic uncertainty and tariff woes could place additional pressure on retailers within its portfolio, potentially affecting rental income and operational performance. Additionally, interest rate sensitivity and elevated leverage ($27.6 billion in debt) remain key concerns in a high-rate environment. Its interest expenses were up 11.5% year over year to $268.4 million in the first quarter of 2025. The estimate revisions reflect a somewhat bullish trend. The Zacks Consensus Estimate for 2025 adjusted funds from operations (AFFO) per share has climbed marginally over the past month, while the same for 2026 has also moved north by a cent over the same time frame. Realty Income stock is trading at a forward 12-month price-to-FFO of 13.41X, below the retail REIT industry average of 15.09X but higher than its one-year median of 13.16X. While Realty Income stock is currently trading at a reasonable discount compared to its industry peer Agree Realty Corporation, it is at a slight premium to NNN. This valuation disparity might not be as favorable as it seems. Agree Realty is trading at a forward 12-month price-to-FFO of 17.45X, while NNN is trading at 12.56X. In conclusion, Realty Income stands out as a premier dividend stock, offering dependable income and solid long-term growth potential. While the stock trades at a discount compared to peers such as Agree Realty, it seems prudent for investors to wait for more macroeconomic clarity before initiating new positions. However, for existing investors