Sterling Rides E-Infrastructure Boom: AI-Driven Data Centers and Strong Execution Drive Growth

Sterling Infrastructure, Inc. (STRL) has capitalized on the surging demand for e-infrastructure, delivering a standout performance in the first quarter of 2025. The company reported an 18% year-over-year revenue increase in its E-Infrastructure Solutions segment, with adjusted operating income surging 61% and margins expanding by more than 600 basis points to 23%. This growth is fueled by rising investments in AI-driven data centers, which now make up more than 65% of Sterling’s e-infrastructure backlog.

Strong project execution and the ability to finish mission-critical projects ahead of schedule have helped Sterling deepen relationships with large customers, reinforcing its competitive position. On the financial front, Sterling posted adjusted earnings per share (EPS) of $1.63, up 29% year over year, and adjusted EBITDA rose 31% to $80 million. The company ended the quarter with a record $1.2 billion in e-infrastructure backlog and future-phase visibility nearing $2 billion, reflecting both demand strength and Sterling’s execution capabilities.

Sterling’s exposure to onshoring trends, such as semiconductor and biopharma facility construction, further amplifies its growth runway. The company’s phase-by-phase pricing model also minimizes risk from raw material and fuel cost fluctuations, helping preserve margins even amid volatility. Looking ahead, management expects mid-to-high teens revenue growth for the E-Infrastructure segment in 2025, with adjusted operating margins continuing in the mid-20% range.

While Sterling boasts superior margins and backlog momentum, it faces competition from peers like Quanta Services (PWR) and EMCOR Group (EME), which also target high-growth sectors like data centers, semiconductors, and transportation buildouts. Both Quanta Services and EMCOR offer broader national footprints and diversified customer bases, keeping competitive pressure intense in this expanding market.

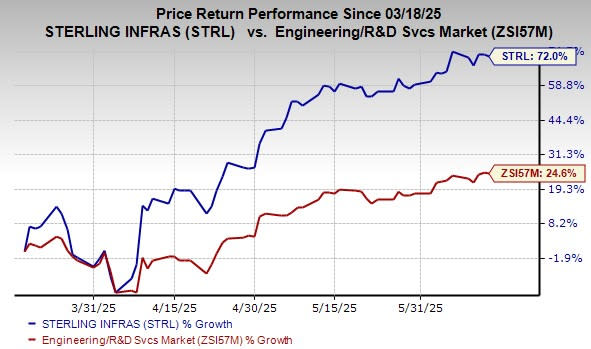

From a valuation standpoint, Sterling is currently trading at a premium with a price-to-earnings ratio of 22.7X compared with the industry’s average of 20.54X. The Zacks Consensus Estimate for Sterling’s 2025 and 2026 EPS estimates have moved upward over the past seven days, indicating 40.3% and 9.7% year-over-year growth, respectively. STRL stock currently carries a Zacks Rank #2 (Buy).

Sterling takes off with the E-Infrastructure surge: Its AI powered data centers and robust execution strategies precisely propel growth in a competitive digital landscape.

The remarkable expansion of Sterling amidst the e-infrastructure boom is a testament to their strategic deployment of AI powered data centers and unwavering commitment towards execution excellence, fueling sustainable growth in today's digital landscape.

The meteoric rise of Sterling看到其通过人工智能驱动的数据中心与卓越的执行能力,正引领着电子基础设施的繁荣发展之路。