Is THOR Industries a Good Time to Buy for New Investors?

THOR Industries, Inc. (THO), the largest manufacturer of recreational vehicles (RVs) in the world, has recently retired its prior share repurchase authorization and approved a new one, allowing for the repurchase of up to $400 million of its common stock. This move reflects the company's strong financial position and commitment to shareholder returns. However, despite a strong fiscal third quarter, THOR faces several near-term challenges that investors should be aware of.

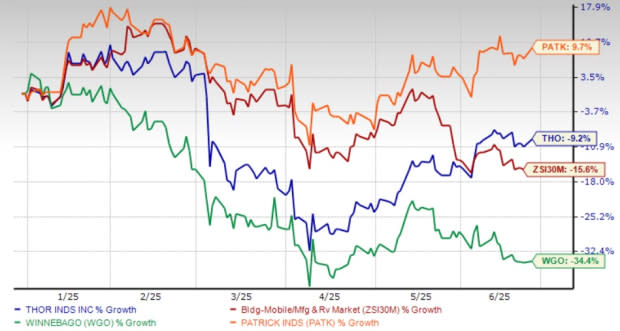

YTD Price Performance

The year-to-date (YTD) performance of THOR has been mixed. While the company and its industry have declined by 9.2% and 15.6%, respectively, shares of Patrick Industries, Inc. (PATK) have risen by 9.7%. This variation in performance highlights the need for investors to carefully consider the individual factors affecting each company in the industry.

Undervalued Compared to Industry

With a forward 12-month price-to-sales (P/S) ratio of 0.47, THOR looks undervalued compared to the industry ratio of 0.67. This suggests that the market may be underestimating the company's potential for growth and profitability.

Strategic Acquisitions and Expansions

THOR's market position has been fueled by strategic acquisitions such as EHG and TiffinHomes, which have brought commercial synergies and expanded its product portfolio. The acquisition of Airxcel strengthens the supply chain and diversifies revenues, especially in the aftermarket business. Additionally, THOR is expanding its revenue streams beyond its core RV segments through initiatives like RV Partfinder, which improves the customer and dealer experience by reducing repair cycle times and enhancing service efficiency.

Challenges Ahead

Despite a strong fiscal third quarter, THOR expects margin pressures to persist due to weaker retail and wholesale demand in North American Motorized and European segments. The company expects the fiscal 2025 consolidated gross profit margin to be in the range of 13.8-14.5%, compared to 14.5% recorded in fiscal 2024. The upcoming model year transition and changing macroeconomic conditions have resulted in a decline in THOR's backlog, which doesn't bode well for its sales. Additionally, substantial investments in automation and innovation strategies are expected to increase SG&A expenses as a percentage of sales, exerting pressure on profit margins.

Conclusion

While THOR's new $400 million share repurchase authorization reflects its strong financial position and makes it an attractive choice for existing investors, it doesn't necessarily mean it's the right time to buy the stock for new investors. The company anticipates continued margin pressure due to weaker demand and a shrinking backlog, which may weigh on profitability. For existing investors, THOR's expanding revenue stream and commitment to shareholder returns offer reasons to hold the stock. However, for new investors, a wait-and-watch approach looks like a more prudent choice. Currently, THOR carries a Zacks Rank #3 (Hold).

Investors should carefully consider the individual factors affecting each company in the Zacks Building Products - Mobile Homes and RV Builders industry before making any investment decisions. It's important to stay informed and up-to-date with the latest news and analysis to make informed investment choices.