The J. M. Smucker Slides 12% in a Month: How to Play SJM Stock

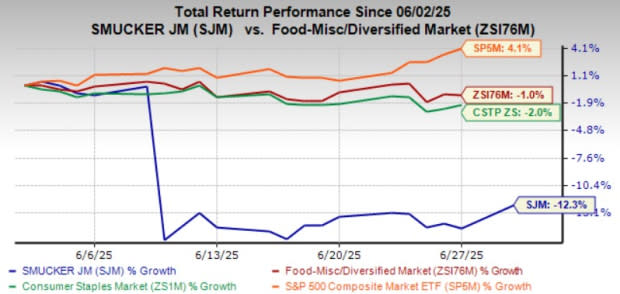

The J. M. Smucker Company SJM has seen its shares plunge 12.3% over the past month, significantly underperforming the industry’s modest 1% decline and the S&P 500’s 4.1% growth. The stock also lagged behind the broader Zacks Consumer Staples sector, which fell 2% during the same period. This sharp pullback reflects a mix of broader macroeconomic challenges and company-specific headwinds.

The J.M. Smucker also underperformed some of its peers, such as The Hershey Company HSY, McCormick & Company, Incorporated MKC and General Mills, Inc. GIS. Shares of Hershey and McCormick have gained 2.8% and 3.2%, respectively. In contrast, General Mills saw its stock decline 4.3% in the past month.

Investors remain divided on whether The J.M. Smucker is poised for further downside or approaching a potential rebound.

SJM Price Performance vs. Industry, S&P 500 & Sector

Zacks Investment Research

Zacks Investment Research

Image Source: Zacks Investment Research

As of the last trading session, SJM closed at $98.20, near its 52-week low of $93.30, attained on June 18, 2025. The J.M. Smucker stock is trading below critical technical thresholds, including its 50 and 200-day moving averages.

SJM is currently trading at a discount to both its historical averages and industry peers, largely due to its recent share underperformance. The stock's forward 12-month P/E ratio stands at 10.44, below its one-year median of 11.07 and well below the industry average of 15.85. While the lower valuation may reflect perceived risks, it also underscores the market’s cautious sentiment, especially when compared to peers like Hershey, McCormick, and General Mills, which are trading at significantly higher multiples of 27.02X, 23.81X and 13.94X, respectively.

SJM P/E Ratio (Forward 12 Months)

Zacks Investment Research

Image Source: Zacks Investment Research

What’s Weighing on The J.M. Smucker’s Growth?

The J.M. Smucker is contending with a series of strategic and operational headwinds, the most pressing of which centers on its underperforming Sweet Baked Snacks segment, led by the Hostess brand. In the fourth quarter of fiscal 2025, the segment reported a 14% decline in comparable sales, driven by sluggish consumer demand amid persistent inflation and diminished discretionary income. These external pressures were compounded by internal missteps in distribution, merchandising, and execution, further weighing on performance.

Another significant challenge is the surge in green coffee prices, which have reached record highs. This inflationary trend forced SJM to implement multiple price increases across its coffee portfolio. While the company managed to preserve margins through responsible pricing, it faces an increasing risk of volume loss due to demand elasticity. This issue is further complicated by tariffs on imported green coffee, mainly sourced from Brazil and Vietnam, adding further margin pressure.

The J.M. Smucker’s pet food segment also showed signs of stress. Net sales declined 13%, hit by retailer inventory reductions and weak demand for dog snacks. Although Meow Mix showed some resilience, the broader category remains soft as consumers cut back on discretionary spending.

SJM faces exposure to global trade tensions, particularly via tariffs and regulatory changes. Though much of its production is U.S.-based, key inputs like green coffee are subject to import duties. As a result, the company is actively exploring alternative sourcing and pricing strategies to mitigate these risks. Nevertheless, external volatility remains a structural headwind.

Looking ahead, the company has issued a cautious outlook for fiscal 2026. SJM expects adjusted earnings in the range of $8.50 to $9.50 for the full year, which includes material headwinds from coffee elasticity, increased marketing investments, tariff impacts, and continued weakness in the Sweet Baked Snacks segment. Notably, in the first quarter of fiscal 2026, adjusted earnings are expected to decline approximately 25% year over year, reinforcing concerns about near-term margin pressure.

The J.M. Smucker Estimates: Trouble Still Brewing?

Reflecting cautious sentiment around The J.M. Smucker, the Zacks Consensus Estimate for earnings per share (EPS) has seen downward revisions. Over the past seven days, the consensus estimate has declined for the current quarter by 10 cents to $9.28 per share and fiscal year by 15 cents to $9.99 per share. (Find the latest EPS estimates and surprises on Zacks Earnings Calendar.)

Zacks Investment Research

Image Source: Zacks Investment Research

Here’s How to Play SJM Stock

The J.M. Smucker Company is navigating a difficult environment marked by weak consumer demand, rising commodity costs, tariff headwinds, and underperformance in key segments, such as sweet baked snacks and pet food. These challenges have been compounded by internal execution issues and downward revisions to earnings estimates, signaling growing investor concern. The stock has also fallen below key technical support levels, reflecting continued bearish sentiment. With limited near-term growth catalysts and ongoing margin pressures, SJM’s outlook remains unfavorable. Investors may be better served by exploring more stable opportunities. SJM currently has a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Hershey Company (The) (HSY) : Free Stock Analysis Report

General Mills, Inc. (GIS) : Free Stock Analysis Report

The J. M. Smucker Company (SJM) : Free Stock Analysis Report

McCormick & Company, Incorporated (MKC) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks Investment Research

![What is a customer journey map and how to make your own [examples included]](https://www.antiochtenn.com/zb_users/upload/2025/07/20250703080832175150131270552.png)