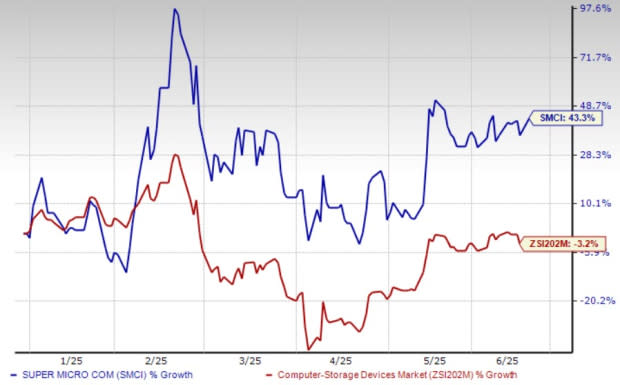

Super Micro Computers Rising Server Demand: Can Its Innovations Keep Pace with Market Growth?

Super Micro Computer (SMCI) has reported a significant 19% year-over-year increase in revenues for its server and storage system segment in the third quarter of fiscal 2025, crossing the $4.5 billion milestone. This impressive performance is driven by the increasing demand for the company's innovative products among hyperscalers and AI clients, with the segment accounting for 97% of the company's total revenue.

The company's direct liquid cooling products for data-center applications have reached a production volume of over 2000 DLC racks per month, contributing to the growth of the server and storage system segment. SMCI's recent product launches, including its Data Center Building Block Solutions (DCBBS) and petascale storage systems for AI workloads, are expected to further boost the segment's performance in the future.

In addition to its product innovations, SMCI is also expanding its global manufacturing footprint across Malaysia, Taiwan, and Europe to ramp up the deployment of its server and storage solutions while mitigating geopolitical and tariff barriers of local governments. The Zacks Consensus Estimate for SMCI's fiscal 2025 revenues is $22.12 billion, indicating a 48% year-over-year growth.

The global storage and server market is dominated by players like Pure Storage (PSTG) and Hewlett Packard Enterprise (HPE). Pure Storage provides a range of modern storage solutions through its offerings like FlashArray, FlashBlade, and Pure Cloud Block Store, while HPE offers a range of server services, including HPE ProLiant, HPE Synergy, HPE BladeSystem, and HPE Moonshot servers. In the second quarter of fiscal 2025, HPE's server segment sales grew 6% year over year due to strong demand for its AI servers.

According to a report by Mordor Intelligence, the enterprise server market is expected to grow at a CAGR of 8.03% from 2025 to 2030 and reach $139.81 billion. Players like Super Micro, Pure Storage, and HPE are poised to witness tremendous growth given the huge opportunity in the space.

From a valuation standpoint, SMCI trades at a forward price-to-sales ratio of 0.87X, down from the industry's average of 1.61X. The Zacks Consensus Estimate for SMCI's fiscal 2025 earnings implies a year-over-year decline of 6.33%, while the same for fiscal 2026 indicates growth of 35.75%. Despite these mixed signals, SMCI currently carries a Zacks Rank #4 (Sell).